Become an insider!

Get our latest payroll and small business articles sent straight to your inbox.

In this Article:

When should you create a succession plan for your business?

There’s no time like the present.

That may not be the answer you were looking for. In fact, many smaller businesses and partnerships don’t consider the importance of succession planning until a senior-level partner or owner becomes incapacitated, or until a partnership dissolves.

Business-changing events like these put the limelight on future plans and the importance of knowing what will happen if…

This is especially important for smaller businesses.

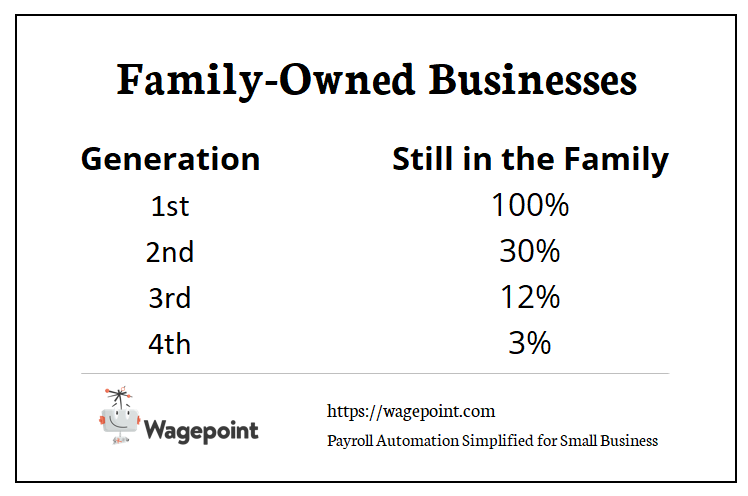

Although family-owned businesses, for example, account for 64% of US gross domestic product, only 30% remain in the family by the second generation, decreasing to 12% by the third generation and 3% by the fourth generation.

Meanwhile, among Canadian family-run and small businesses, 95% indicate that succession plans are key to securing their future in the long run.

Corporations enjoy a larger safety net for recovery and succession when valuable senior-level players are removed from the running. Smaller businesses and partnerships must create a succession plan to survive in the long-term, remembering that the plan should adapt depending on growing business needs and changing conditions.

Here are 5 rock-solid steps for creating a viable succession plan for your organization.

1. Select Your Successor

- Where should you look for your replacement?

- Is there a way to get objective help making the decision?

It’s a good idea to look within your organization to handpick candidates with the proper experience and leadership skills.

Searching internally provides several benefits: The candidate already knows the business. You’ve watched their growth, so you can be sure they’ll fit the role. And you can tailor a succession plan to suit their growth as well as the company’s.

Of course, it may be overwhelming to choose your replacement from within so small a pool, and you may worry that it will disrupt the “work family” environment you’ve worked so hard to cultivate.

If that’s the case, it may help to hire an objective third-party business consultant. Their outside perspective can make it easier to weigh options objectively. Keep in mind, though, it should inform your decisions, not serve as the sole source of your ultimate decision.

Ideally, you’ll start the succession selection process well before you plan to retire or otherwise depart. According to Thomas Collura, partner and attorney at Hodgson Russ, succession planning should ideally begin before an owner starts the business.

“That’s the time to consider how ownership and management will be transferred in the event of death, disability, or termination of employment.”

The business type and formation will ultimately influence how the succession takes place, says Collura.

“For corporations, the succession plan for director and officer transition is typically set forth in the By-laws and any restrictions, options, or other requirements concerning the transfer of a shareholder’s ownership, during life or upon death, would be set forth in a Shareholder Agreement.

“For LPs or LLCs, these issues are typically addressed in the Partnership Agreement (for LPs) or Operating Agreement (for LLCs). Obviously, the terms of these documents will evolve and may change over time.”

Collura also states that the biggest mistake is failing to have a plan or failing to revisit it. So, whether you’ve already put together a succession plan or not, it’s time to start thinking about it again.

Once you know who the successor will be, begin the training process at least a decade in advance. Understanding the ins and outs of even a small organization takes time, and your successor should grow into their duties. Let them make mistakes now, instead of later when more is on the line.

2. Identify Goals for Yourself

- What personal goals for retirements and cash flow do you have or require?

- Have you upped your retirement account contributions to their fullest limits?

- Is this something you’ve discussed with your family? Don’t leave out health concerns or travel goals.

Give serious thought to your final months or years leading the organization. What do you hope to accomplish during that time or leave behind as your legacy? What steps have you taken toward these goals?

Make both a personal and professional game plan for what you’ll leave behind and what you’ll pursue.

As you identify a timetable for the succession, gradually reduce your professional duties to ease into more personal ones. This will make the transition easier on everyone and help you identify the right time to begin succession training and transitioning.

3. Identify Goals for the Company

- How do past and present developments affect the future of the company and its mission?

- What plans will you soon set forth that others will need to carry out in the future?

- Are you okay with your successor choosing a different route based on their experience and training, or do you wish to remain involved indirectly for a few years as a consultant or in a similar capacity?

Don’t hesitate to develop a panel of advisers from inside and outside the company as you identify goals for the company. Lawyers and accountants can offer essential and legal advice as you work through these questions.

It’s a good idea to decide in advance how disputes will be resolved, whether mediation or finding a third party to judge.

Be sure to document all visions and goals in the budding succession plan.

3. Identify the Critical Company Functions

- What are the critical functions of your company?

- Can lower-priority duties be assigned to senior-level employees, so the successor can focus on only the most critical company functions?

In many cases, leadership roles evolve to fit the people in those roles. The successor will bring an entirely new set of skills to the role and may more than fill the expectations in one area while falling short in another.

It’s important to evaluate those differences now, while you’re in the planning stages.

Identify the functions that the successor should take on and subsets of duties that could be delegated. By putting these options into the succession plan now, it will be more accurate and flexible, which will ensure a successful transition.

4. Grow a Formal Training Program

- What skills can the successor adapt to quickly through learning to lend confidence?

- Would a formal training program help the successor step into the role?

- Are there people in the organization who should assist with training?

Once you know what skills are critical to running the company, it’s time to set priorities for training the successor.

Identify the heads of relevant departments who may assist in the succession training. You may also let them help you and the successor develop a long-term vision for the company.

Encourage cross-training in various departments, including competency in administration, operations, sales, customer service, and marketing.

Now is a great time to offer mentoring opportunities to all employees to cultivate an environment of continuous learning. Of Fortune 500 businesses, 71% offer mentoring programs to employees, and small business employees deserve no less. Imagine the boost in innovation and learning a mentor can give to a smaller team!

5. Decide When the Moment of Succession Should Happen

- How long should it take to complete the successor’s training?

- What milestones need to happen before the transition takes place?

When you develop the timetable for succession, consider all aspects of necessary training and realize that the process will be gradual.

Consider carefully what will give you the most confidence at each stage of succession to “hand over the keys.” This will build the successor’s confidence as well.

Do your best to make the transition a smooth one, but know that no road to success or succession is without its bumps. Installing your successor during your lifetime is much easier than departing and leaving all the pieces up in the air for confused team members and senior-level employees to catch.

Other Nuts-and-Bolts Strategies for Succession Planning

Strategizing a succession plan in terms of vision and cross-training is one thing, but other nuts and bolts must be considered as well.

Take time to consider all your financial options so your organization can thrive, especially if it’s in a small niche or highly competitive market.

Will You Sell Your Business Interest?

As you plan for the future, consider whether you’ll sell your business interest in exchange for particular assets or cold hard cash.

Many company officers, partners, and owners have the option to sell before retirement, at the time of death or during the interim. Keep in mind that you may be required to pay a capital gains tax if you sell your business interest before death.

Don’t Forget a Buy-Sell Agreement

A buy-sell agreement is a legal contract that arranges the selling of business interest ahead of time. The contract outlines a particular, predetermined event that will trigger the sale, such as a divorce, disability, retirement, or death.

When the event is triggered, the buyer must pay for the interest at fair market value. Without this agreement, the buyer could end up with a huge tax burden.

Establish a GRAT or GRUT

Plan for a smooth succession by establishing Granter Retained Annuity Trusts (GRATs) or Unitrusts (GRUTs), which serve as irrevocable trusts that transfer assets. Income is still made for a period, but at the end of the period, the trust’s assets go to the beneficiaries. Death also triggers the dispersal.

Plan for a Private Annuity

A private annuity may help you provide for your long-term needs and those of your family. A private annuity is conducted through the sale of a property in return for regularly occurring payments over the course of your life.

The annuity transfers ownership of the company to the buyer, who then pays you on a regular schedule until you die. A surviving spouse can also sometimes be included, which would avoid estate or gift taxes.

Consider Self-Canceling Installment Notes (SCINs)

Owners may transfer a company to the buyer through self-canceling installment notes (SCINs). The buyer takes on a promissory note, obligating him or her to make a number of payments to the original owner. Leftover payments cancel upon the death of the seller.

Keeping It in The Family Limited Partnerships

Happen to own a family-run business and torn about whether to pass it on or sell it to an outside party?

If you decide to go the route of an inherited business, keep it in the family by forming a family limited partnership. You’ll establish a partnership with limited and general partnership interests, and you’ll then transfer the business over to the partnership. Over the course of a few years, you can offer your business interest as a gift to your family.

Final Thoughts

Know that once you’ve made the succession plan, it can change. New circumstances, unforeseen needs, or a new vision can all inspire changes to your finished plan.

The good news is you can change course and make corrections as you go, especially if you see any vital errors. But you must also trust in the training process and in your successor’s decisions.

So relax. You have to give up the reins sometime. Let go of the responsibilities of leadership, and look toward your future.

Decide what legacy you want to leave behind, both professionally and personally, and greet it with promise and hope by making a rock-solid succession plan.

People often say change is inevitable, but it is possible to cultivate a change for the better by planning in advance for your business succession.

The advice we share on our blog is intended to be informational. It does not replace the expertise of accredited business professionals.