Become an insider!

Get our latest payroll and small business articles sent straight to your inbox.

In this Article:

This blog post is written for Canadian businesses.

Click here for How to Handle Taxes on Bonus Wages for US companies.

As exciting as bonus payouts can be for your employees, for most of them, it’s a bittersweet payment because of the amount that is paid out in taxes.

While those concerns are valid, they are slightly exaggerated.

Canada Pension (CPP) and Employment Insurance (EI) are mandatory deductions on a bonus payment with one exception — when an employee has contributed the maximum yearly amounts for CPP and/or EI, no further deductions will occur.

Income tax, on the other hand, is required unless the bonus is being allocated to an RRSP.

When this option is chosen, the net amount (after CPP and EI are deducted) can be put into the employee’s RRSP — providing they have room in their yearly contribution limit.

How does the bonus tax method work in payroll?

The best way to answer this question is by contrasting it with the normal rules for calculating Canada Revenue Agency (CRA) income tax source deductions, termed the periodic method.

There are other CRA tax methods — the lump-sum and TD1X methods — but the periodic method is the one closest to the bonus method itself.

For the discussion in this post, we will focus on comparing and contrasting the periodic and bonus methods for calculating income tax on bonuses.

The Periodic Method vs. The Bonus Method

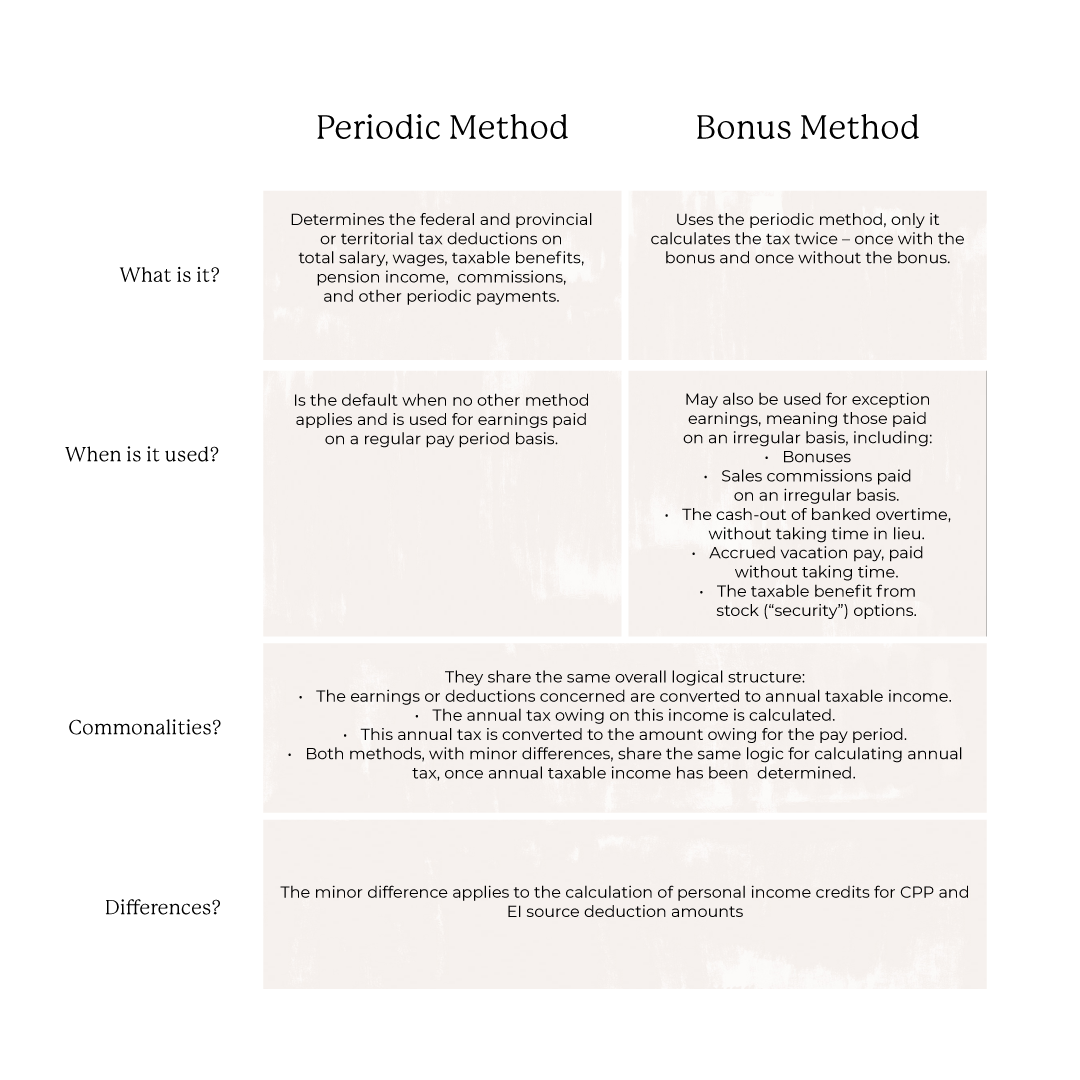

The periodic method determines the federal and provincial or territorial tax deductions on total salary, wages, taxable benefits, pension income, commissions, and other periodic payments. The periodic method is the default when no other method applies and is used for earnings paid on a regular pay period basis.

The bonus method uses the periodic method, only it calculates the tax twice – once with the bonus and once without the bonus. The bonus method may also be used for exception earnings, meaning those paid on an irregular basis, including:

- Bonuses

- Sales commissions paid on an irregular basis.

- The cash-out of banked overtime, without taking time in lieu.

- Accrued vacation pay, paid without taking time.

- The taxable benefit from stock (“security”) options.

For example, when employees work overtime and are paid for that overtime in the same pay period, the periodic method applies. The same is true when employees are subsequently given time in lieu. The bonus method only applies to overtime that’s banked and then subsequently paid out, only as cash, such as on termination.

There are two things that the bonus and periodic methods share in common.

First, they share the same overall logical structure:

- The earnings or deductions concerned are converted to annual taxable income.

- The annual tax owing on this income is calculated.

- This annual tax is converted to the amount owing for the pay period.

Second, the bonus and periodic methods, with minor differences, share the same logic for calculating annual tax, once annual taxable income has been determined.

**The minor difference applies to the calculation of personal income credits for CPP and EI source deduction amounts, but we won’t go into that level of detail here.**

To keep it simple, we’ll limit our example to showing just the federal tax portion of the bonus calculation.

To keep it simple, we’ll limit our example to showing just the federal tax portion of the bonus calculation.

Here are the details we need to perform the payroll calculations shown in this post:

(The data used in this post is for one specific example. You’d use similar variables in your own calculations, accommodating for salary or hourly, bonus amount and frequency, pay frequency, tax claim codes, CPP and EI exemption, etc. relevant to your employees and your company.)

-

Rate of Pay: Employee receives a $1,600 salary every pay.

-

Bonus Amount: Employee is receiving a (one-time) bonus of $5,000 on this pay. (If the employee had a previous bonus within the year or will receive others, these will also need to be taken into account.)

-

Pay Schedule: Employee is paid bi-weekly. (You would need to enter the payroll frequency that’s appropriate for your company, monthly, weekly, bi-weekly, semi-monthly.)

-

Claim Code: Federal tax claim codes is 1 (basic).

-

Withholding Status: Employee is CPP and EI exempt.

-

Employment Credit: The Canada Employment Credit does not apply.

-

Annual Tax Owing Rate: The Annual Owing Tax Rate in this example is for Ontario. (In doing your own calculations, you’d have to select the appropriate province.)

-

Tax Year: Tax year is 2018 for this example. (For accuracy, use the appropriate tables/rates for your tax year.)

|

Payroll Bonus Tax Calculation Examples |

|||||||||||||||||

|

|||||||||||||||||

|

Example Two – Bonus Method |

|||

|

Step |

Federal Income Tax Calculation |

Period with Bonus |

Periodic without Bonus |

|

1 |

Multiply pay period earnings times the number of periods per year, $1,600 times (26 pay periods for bi-weekly payroll). |

$41,600 |

$41,600 |

|

Add the current bonus. |

$5,000 |

|

|

|

Total annual taxable income |

$46,600 |

$41,600 |

|

|

2 |

Calculate the annual tax owing, at 15%, less $0 (refer to section A on CRA chart T4032). |

$6,990 |

$6,240 |

|

3 |

The tax owing is the difference between the 1st and 2nd results. |

$750 |

$240 |

Using the periodic method, the total amount the employee would pay in taxes would be $1,451.54, while the bonus method the tax paid would be $990.00 ($240.00 on their salary plus $750.00 on the bonus).

So, using the bonus method it lowered the federal tax on the bonus by $461.54.

While Wagepoint uses the periodic method for calculating taxes on bonuses, the CRA’s Payroll Deductions Online Calculator (PDOC) provides an easy workaround to calculate taxes on the bonus using the bonus method in order to reduce the tax contributions for you and your employees. Contact the Wagepoint support team if you need assistance adjusting taxes on the bonus for your payroll.

And, that’s bonus taxation in a nutshell.

This post was produced in collaboration with Alan McEwen, a Vancouver Island-based HRIS/Payroll consultant and freelance writer with over 20 years of experience in all aspects of the industry.

Additional reads.

- Giving an Employee Bonus — What You Need to Know [Infographic Included]

- Payroll Tax vs. Income Tax — How They Work for Canadian Payroll

- A Canadian Small Business Employer’s Guide to T4s, T4As and RL-1s [Checklist Included]