Become an insider!

Get our latest payroll and small business articles sent straight to your inbox.

In this Article:

Most enforcement of government payroll regulation is reactive, initiated by an employee complaint. Similarly, while the possible penalties for non-compliance can theoretically be severe – including potential jail sentences – such penalties are rarely, if ever, imposed.

However, there is one area of government regulation where significant penalties, at least financial ones, are actively and regularly imposed.

These are penalties for employers who fail to remit CRA source deductions within the required due dates.

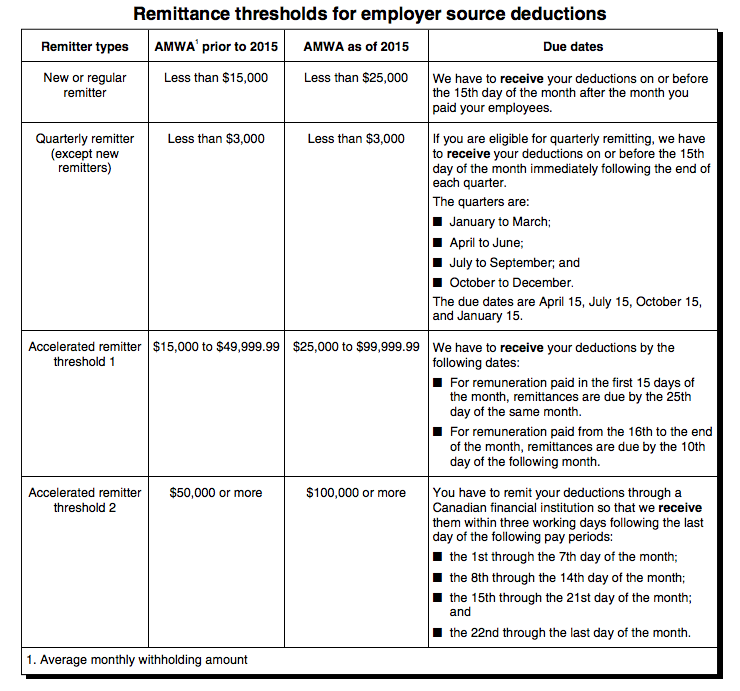

The default due date for CRA remittances is the 15th of the month following. For example, November 15 is the default due date for employee direct deposits dated October 2.

This default applies until the start of the 3rd tax year in which the employer is required to make remittances. For example, if an employer is first required to make remittances for the month of November 2015, the default monthly due dates apply until remittances for the first month of the 2017 tax year.

Starting with this 3rd tax year, the CRA assigns due dates based on each employer’s monthly average remittance, calculated based on the remittances 2 years prior.

For example, due dates for 2017 are based on the average monthly remittance for 2015. However, if the immediately prior year is more favorable, employers can contact the CRA (the phone number is given on page 44 of the 2015 Employers’ Guide, T4001) to have remittance due dates based on this year instead.

Related: What You Need to Know About Your Payroll Remittance Schedules

Related: What You Need to Know About Your Payroll Remittance Schedules

CRA monthly average remittances are calculated by dividing income tax, CPP and EI remittances, for the year concerned by a default 12. If the employer wasn’t liable to make remittances in all 12 months concerned, use the number of months remittances were required.

For example, if a business operates only from May to October, the monthly average is calculated by dividing remittances for the year by six. This also applies to employers who start operations midway through a tax year.

There are also special rules for associated corporations – corporations controlled by shareholders that don’t deal at arm’s length. This could be a parent and its wholly-owned subsidiaries or a group of corporations controlled by related persons, such as a husband and wife.

Associated corporations share common CRA remittance due dates, based on a single monthly average calculated from all remittances for the associated corporations.

Based on these rules, the following table shows the four remittance frequencies that apply for CRA source deduction purposes:

The due dates described above are adjusted for Saturdays, Sundays, statutory holidays and other non-banking days (see the list of non-banking days maintained by the Canadian Payments Association).

These adjustments are of two different types.

For quarterly, monthly or Threshold 1 remitters, if the 10th, 15th or 25th falls on a non-banking day, the remittance is due the next banking day.

For Threshold 2 remitters, where remittances are due within 3 days after the end of each remittance period, any non-banking day within this 3 day limit doesn’t count.

For example, June 15, 2013, was a Saturday. Remittances otherwise due that day were not late if they were paid on June 17, 2013.

Similarly, September 14, 2013, was a Saturday. Three business days after was Wednesday, September 18, 2013. Threshold 2 remittances for the 2nd remittance period in that month were not late if they were paid on the 18th.

CRA can assess a penalty when remittances are received later than the scheduled due date.

The penalties are:

- 3% if the amount is one to three days late;

- 5% if it is four or five days late;

- 7% if it is six or seven days late; and

- 10% if it is more than seven days late, or if no amount is remitted.

Fines for failing to remit CRA source deductions are avoidable. Follow the schedules above to keep fines off your yearly and monthly budgets.

Disclaimer: The advice we share on our blog is intended to be informational. It does not replace the expertise of accredited business professionals.